NORTHEAST FLORIDA — It’s a stressful time to be in the market for a home. Excessively high prices are impacting affordability for millions of Americans, and Florida is no exception. In fact, a recent study from Florida Atlantic University found that the top five overvalued real estate markets in the country right now are in the Sunshine State.

High prices aren’t the only hurdle facing potential homebuyers. Other obstacles include lack of inventory, bidding wars, and not having enough cash on hand for a down payment—putting the dream of homeownership even further out of reach for millions of people.

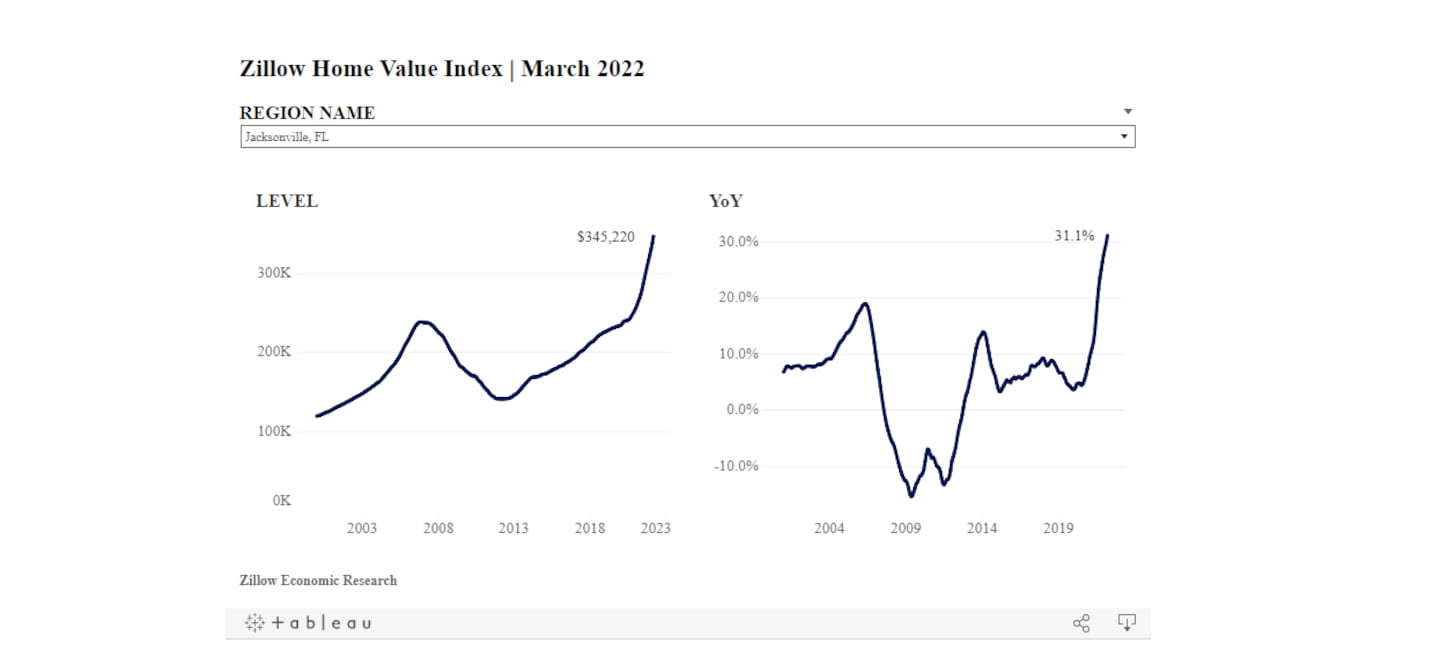

So what’s the latest on the situation here in Northeast Florida? A new report from the Northeast Florida Association of Realtors breaks down the market conditions county-by-county. The biggest takeaway? Home prices are still on the rise.

PRICED OUT OF JAX: Jacksonville’s rental crisis featured on 60 Minutes

According to the report, there were 2,724 single-family homes for sale in April—an almost 20% drop from what was on the market a year ago. The median price of single-family homes was reported at $380,000, a 2.3% increase since March and a nearly 24% rise from a year before.

“There is not much negotiating room for buyers with just over 100% of list price received and nearly 42% of homes selling over list price,” says Mark Rosener, president of NEFAR. “Buyers must be prepared to make a strong offer right from the start.”

The Housing Affordability Index—which measures whether or not a typical family earns enough money to qualify for a mortgage loan on a typical home at the national and regional levels based on the most recent monthly price and income data—fell to 82 from 84 in March. That means nationally, the median household income was only 82% of what is necessary to qualify for a median-priced home under prevailing interest rates. Locally, affordability indexes vary from county to county.

DUVAL COUNTY

In Duval County, the April median price of single-family housing was $340,000, up 3% since March 2022. The average number of days on the market was 12, with 42.9% of sales closing above asking price and 100.9% of sellers receiving list price. Active inventory for the county was 1,413 homes, an increase of 4.1% from last month and a 1.2 months supply.

The Home Affordability Index registered at 91 down 3.2% from March.

CLAY COUNTY

In Clay County, the median price of single-family homes rose to $358,495, an increase of 3.9% from March to April. Listings were on the market for an average of 13 days. All sellers received their asking price with 45.6% of sellers closing over list price, a 15.8% increase from March.

The affordability index was 86.5, falling below 100 for the third time in recent memory. There were 347 active listings, a drop of 2.5% from March.

ST. JOHNS COUNTY

The median price of single-family homes in St. Johns rose 2%, from $567,927 in March. The number of days a listing was on the market fell from 16 to 12, and the active inventory rose to 639 homes, a 15.8% increase. 101.2% of sellers received the list price and 41.1% got more than the list price.

The affordability index fell slightly to 55, demonstrating that St. Johns remains the least affordable area to live in Northeast Florida.

PUTNAM COUNTY

Putnam County is the most affordable area in Northeast Florida, with the median price of a single-family home being $201,000, down 10.1% from last month. Homes stayed a median of 26 days on the market in April. Nearly all sellers – 95.9% received their asking price with 21.5% selling their homes for more than the list price, an increase of 39.2%.

Putnam County’s Home Affordability Index registered at 154, making the county over 10 points more affordable than the month before.

NASSAU COUNTY

In Nassau County, the median price of single-family homes was $386,250 in April, a 1% drop from the month before. Listings were on the market for an average of 13 days, down 27% in March. All sellers received their asking price with 32.5% closing over list. Active inventory in March was 159, a 14.4% increase from March.

The Home Affordability Index registered 80.5.

PRICED OUT OF JAX: 25% of all single-family homes in Duval County owned by investment companies

An Action News Jax investigation earlier this year revealed that investment companies are buying up thousands of local homes and keeping them as rental properties—exacerbating inventory issues and creating an “affordability crisis.”

Ishiah Dixon was hoping this year would be it, the year she’d reach her dream of owning her own home. She told us that homeownership has always been a dream of hers, but the local housing market was making that dream impossible.

“We went to go look at a house and they said they marked the houses up $10,000 every time two houses sold. So, we went on Monday, it was in a good budget. We went back and it was marked up 40 grand higher than what we were intending it to be, so we kind of just held off for a little bit,” Dixon said.

At the time of our story, Dixon and her family were renting a home owned by Invitation Homes, a national investment company. It has 429 homes in its local investment portfolio spread across several different corporation names. Using data from the Duval County Property Appraiser, we discovered Invitation Homes isn’t alone or even the biggest player in local real estate investments.

You’ve probably heard of Opendoor, which bought 413 homes in Duval County since 2020. American Homes 4 Rent has tenants in 393 homes and JWB Real Estate Capital has 843 properties.

Duval County Property Appraiser Jerry Holland says this trend is increasing. “We have about 274,000 single-family homes. About 25% of them are owned by investors.”

That means that 25% of single-family homes in Duval County aren’t even owned by families.

Last year, investors bought nearly one in seven homes sold in America’s top metropolitan areas, the most in at least two decades, according to the realty company Redfin. An interactive map on the Washington Post’s website shows the following Jacksonville ZIP codes — ranging from the Westside to the Northside — with the highest percentage of homes bought by investors last year:

1. 54% of homes in 32209

2. 46% of homes in 32208

3. 43% of homes in 32254

Those purchases by private investment companies come at a time when would-be buyers across the country are seeing wildly escalating prices, raising the question of what impact investors are having on prices for everyone else.

“You do have an impact especially when you look at more than 25% of the properties owned by investors. As that number keeps increasing and maybe eventually gets to a third of the properties, they will have an impact on the market as they put them back on the market for sale,” Holland explained.

Various studies have found that corporate landlords are more likely to raise rents, evict their tenants and poorly maintain their properties than smaller landlords. One by the Department of Housing and Urban Development in 2018 found that large corporate owners in Atlanta were 68% more likely than smaller owners to file eviction notices, according to reporting from the New York Times.

Some have tried to compare today’s housing crisis to the one in 2008, but in a report from JP Morgan, market conditions look quite different today from that in the mid-2000s, noting there is currently no place with the same combination of rapid price growth, rapid debt growth, and expanding supply seen in some areas in 2006. Even in states such as New York and California that have high and increasing house prices, there has been no sign recently of the kind of debt growth seen during the boom.

WHAT ABOUT RENTAL PRICES?

The housing crisis has been squeezing local renters too. Over the last year, Action News Jax has received many calls and emails from desperate renters who were facing year-over-year rental hikes of 25% or more.

In March, Zillow reported that the average rent in Jacksonville had soared to $1,719. Just two months later the company reported that rent prices had climbed to the highest numbers it’s ever recorded—hitting an average of $1,904 per month across the country.

While Zillow reports a higher rent for all properties it monitors, the Florida Apartment Association reports a lower average rent in Jacksonville.

According to the Florida Apartment Association:

- For 2020 the average rent in Jacksonville was $1,168

- For 2021 the average rent in Jacksonville was $1,216

- For 2022 the average rent in Jacksonville is $1,435

Rising rents are an increasing driver of high inflation that has become one of the nation’s top economic problems. Labor Department data show rental costs—have made the biggest increase in 20 years, and will likely accelerate.

Economists worry about the impact of rent increases on inflation because the big jumps in new leases feed into the U.S. consumer price index, which is used to measure inflation, according to reporting by the Associated Press.

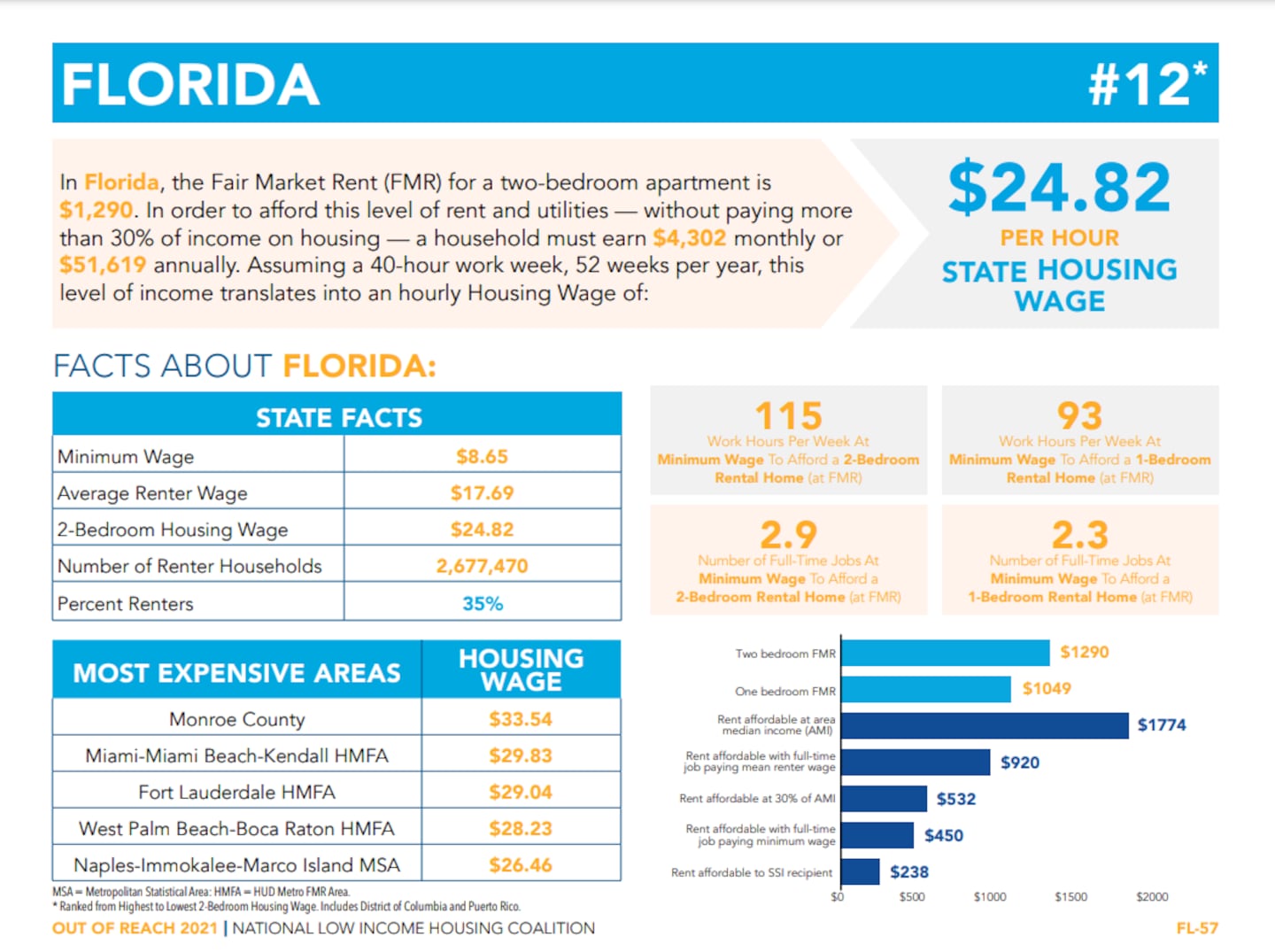

In Florida, a person making $10 an hour, the state’s minimum wage, would have to work 93 hours a week to afford a modest 1 bedroom rental home, according to the latest report from the National Low Income Housing Coalition. In order to afford a 2 bedroom apartment, the average renter in Florida needs to make $51,619, or $24.82 an hour.

Below you can watch 60 Minutes’ Lesley Stahl report on how a lack of construction in the 2010s has created a nationwide housing crisis and the opportunistic Wall Street firms that have stepped in. Jacksonville was a featured city in its report. A young couple facing steep rent rates in Duval County told 60 Minutes they weren’t sure if they would ever be able to afford a home, calling their American dream “unattainable” and “disturbing.”

>> CLICK HERE for more Priced Out of Jax stories

©2022 Cox Media Group